If you run a SaaS company, you’ve been reading a lot of alarming things lately. AI will make your product irrelevant. The “SaaSpocalypse” is here. The era of software subscriptions is over. If even half of this is true, it changes what your company is worth, who will buy fr

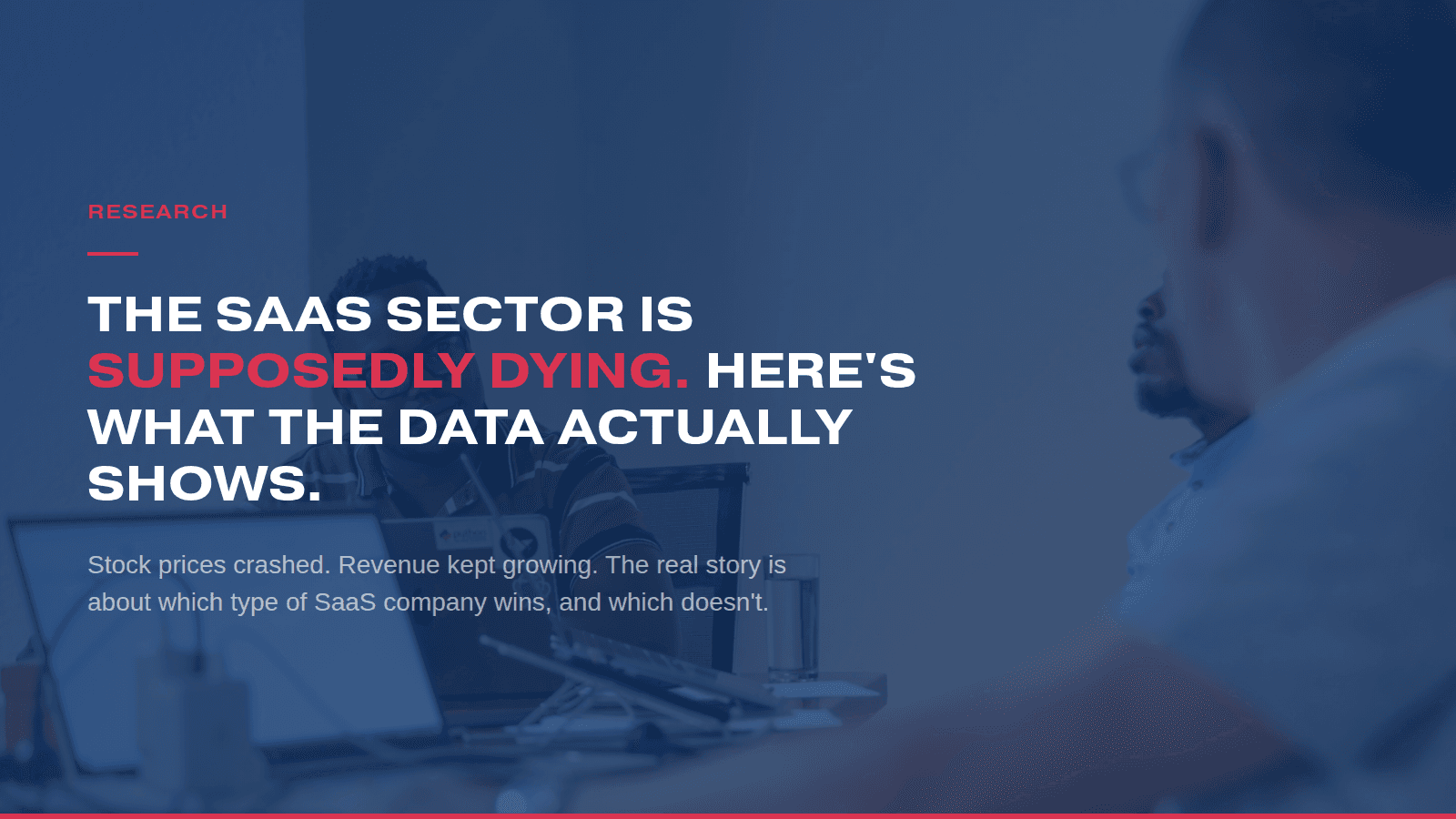

If you run a SaaS company, you've been reading a lot of alarming things lately. AI will make your product irrelevant. The 'SaaSpocalypse' is here. The era of software subscriptions is over. If even half of this is true, it changes what your company is worth, who will buy from you, and whether your team needs to look different a year from now. Three quarters of our clients at Tunga are SaaS companies. So we went and looked at what is actually happening — not the sentiment, the data.

Two sets of numbers

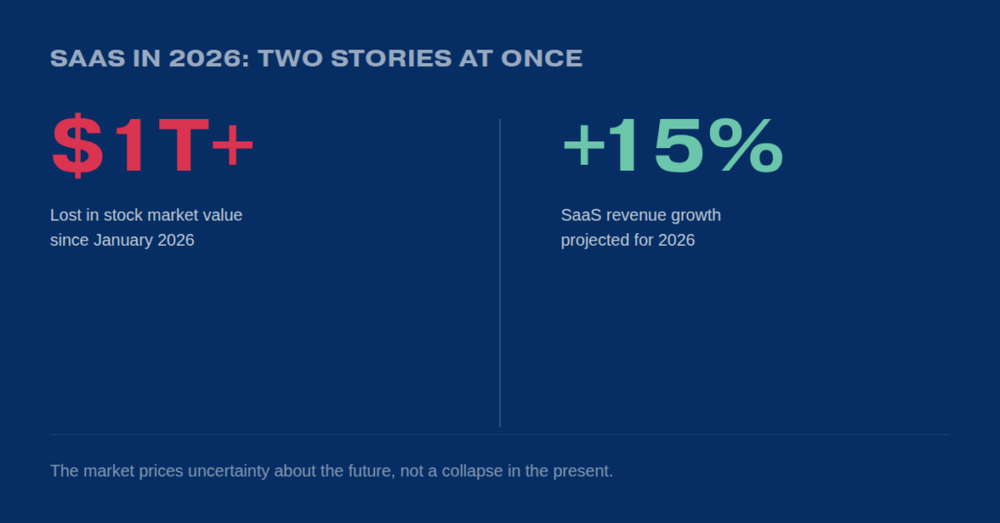

The crash numbers are real. On January 29, 2026 the S&P 500 Software Index dropped 8.7% in a single day. SAP lost over €40 billion in market value. In the first week of February, an estimated $285 billion was wiped out. The total correction is estimated at over $1 trillion.

But there is a second set of numbers. The global SaaS market grew to $408 billion in 2025 and is projected to hit $465 billion in 2026. Gartner forecasts software spending growing 15.2% this year. The average organisation's SaaS spend is up 8% year over year. Stock prices crashing while revenue keeps growing is not a contradiction — the market prices uncertainty about the future, not a collapse in the present.

Not all SaaS is equal

The total market is growing, but underneath that growth, a selection is taking place. The difference comes down to what your product actually does.

One type of SaaS company is essentially a database with an interface on top — simple CRMs, form builders, basic project management. This type is becoming vulnerable. AI agents are increasingly capable of storing, retrieving, and presenting data without needing a separate product.

Another type helps you execute. It manages complex workflows, carries responsibility for compliance or financial logic, and is deeply embedded in how an organisation actually runs. This type is not being replaced, because the cost of getting it wrong is too high. An AI that gives the right answer 6 out of 10 times is not usable for payroll or financial reporting.

Gartner puts a number on this: 35% of simple, single-purpose SaaS tools will be replaced by AI agents by 2030. That's substantial. But it means 65% survives, likely in adapted form.

The model changes, the sector doesn't

The per-seat pricing model is under pressure. When one person with AI support does the work of five, the link between licence count and value breaks. The share of SaaS companies using usage-based pricing has risen from 27% in 2021 to between 38% and 61% today. That is not a sector dying. That is a business model adapting.

The AI tools supposedly replacing SaaS have their own challenges — AI-native products have a median gross retention of just 40%, compared to around 90% for traditional B2B SaaS. Gross margins average 25% versus 75-80%. Both sides of the market are in transition, but the idea that one is simply replacing the other doesn't hold up in the data.

What this comes down to

The SaaS sector is not collapsing. The market is growing, spending is up, and companies that build something deeply embedded in how their clients operate have a strong position. But a selection is happening — between SaaS products that do something hard to take over, and SaaS products that don't. Whether your product manages complexity, executes processes, or carries responsibility that can't afford to be approximate: that's what determines where you sit.